Mieco Chipboard Bhd ("Mieco") is involved in the manufacturing of chipboards.

Mieco has completed its new plant, which led to an increase in its production capacity from 300,000 cu meter p.a. to 940,000 cu meter p.a. The new plant will also enable the company to produce chipboard that meets the European standard i.e. the highest international standard. However, the expansion also coincided with similar expansion by other chipboard manufacturers in Malaysia & around the region (especially, Thailand), which led to a sharp drop in the selling price (due to a jump in supply) & under-utilization of production capacity.

Recent Financial Performance

From the above table, you can see that Mieco’s financial performance was badly affected since QE 30/6/05 when the new plant was completed. The poor selling price coupled with the higher overhead has led to Mieco reporting net losses for 3 quarters i.e. QE31/3/06, QE 31/12/05 & QE 30/9/05.

Mieco has finally turnaround in the last quarter, QE 30/6/06 with a net profit of RM2.9 mil (as compared to a loss of RM0.3 mil in QE 31/3/06) achieved on the back a turnover to RM86.1 mil, which is 27% higher than the immediately preceding quarter’s turnover of RM 68.0 mil. The better result was attributed to improved selling price and increased sale volume as chipboard has benefited from higher selling price of plywood. The sharp rise in the prices of plywood is expected to continue due to sustained rebound in Japanese demand & fall-off in Indonesia logs & plywood supply.

Valuation

Assuming that the performance of Mieco fro the near future shall be similar to that of QE 30/6/06, then the annualized EPS will amount to 5.52 sen. Based on this & Mieco’s closing price of RM0.93 as at Sep 13, the company is now trading at a PE of 16.8 times. This is fairly high but we must bear in mind that future earnings could be better than the last quarter’s earning. In addition, the share price should be well supported by Mieco's high NTA per share of RM1.69. This give the stock a Price to Book of 0.55 times.

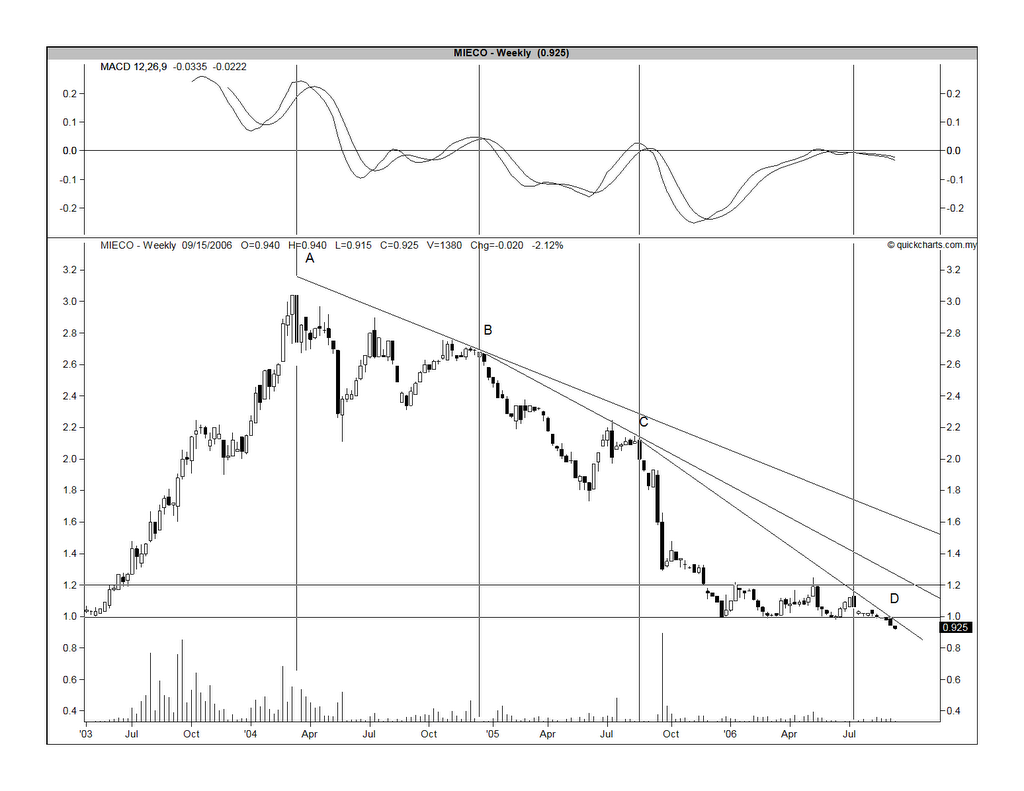

Technical Outlook

From Chart 1 below, you can see that Mieco's share price hit a high of RM3.16 in w/e Mar 12, 2004. Thereafter the stock started to slide. The downtrend accelerated twice; first from December 2004 and then from August 2005. Since January this year, Mieco seemed to have found a support at the RM1.00 level & traded sideway for 8 months. During that period, its prices were range-bound between RM1.00 & RM1.20. 2 weeks ago, Mieco broken below the RM1.00.

Chart 1: Mieco's weekly chart as at Sep 12

From Chart 2 below, you can see that RM0.91/92 level is a good horizontal support level & if that failed, the next levels will be RM0.80 & ultimately, RM0.70.

Chart 2: Mieco's monthly chart as at Sep 13

Weaknesses noted

2 clear weaknesses have been noted:

(1) The technical picture is not good since it has broken below the strong support of RM1.00.

(2) The turnaround is based on 1 quarter of profitable result. It is possible that this performance may not continue.

Recommendation

Based on improving fundamental & attractive price to book, I would recommend Mieco as a LT investment. Slow accumulation would certainly be adviseable as the technical picture is still bearish.

1 comment:

strongly agree with u..

had been accumulating for a year..

company going to announce share buy back

shud push up the share

downside limited

unless poor accounting or fraud like transmile

Post a Comment