Its financial performance has improved considerably since the incorporation of Malayawata’s results as a subsidiary of Ann Joo (in January 2006). Ann Joo's turnover for 2Q2006 ending 30/6/06 has increased 83% q-o-q or 206% y-o-y to RM479 mil. Net profit increased 144% y-o-y to RM18.4 mil but dropped 49.5% when compared to the net profit for the immediately preceding quarter (i.e. 1Q2006). This is because Ann Joo's 1Q2006 ending 31/3/06 has been inflated by the following:

(i) recognition of the net excess of net assets over cost of business combination amounted to RM22.29m following the completion of the conditional voluntary offer by Ann Joo whereby Malayawata becomes a 67.67%-owned subsidiary of Ann Joo; &

(ii) recognition of gain amounted to RM10.41m arising from the completion of the disposal of a piece of leasehold land together with buildings erected thereon.

For details of the last 8 quarterly result, see the table below.

Based the EPS of 9.13 sen for QE30/6/06, we can calculate the full year's EPS to be 36.52 sen. At this EPS & using yesterday (Aug 28)'s closing price of RM1.28, Ann Joo's PE is about 3.5 times. That is very attractive.

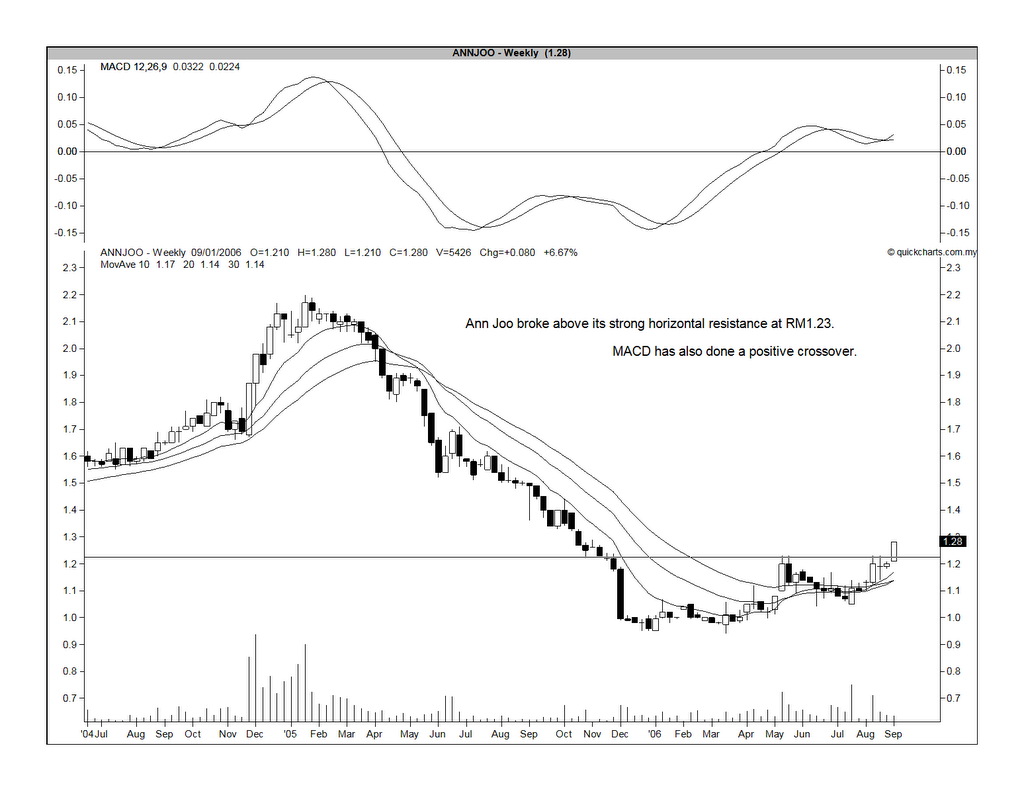

Yesterday, Ann Joo has broken above a very strong horizontal resistance of RM1.23, to close at RM1.28. At the time of writing this post (10.00 a.m.), it is at RM1.32. The first target is about RM1.40 but longer-term, I think this stock can still go higher (see the weekly & daily charts below).

Chart 1: Ann Joo's weekly chart as at August 28

Chart 2: Ann Joo's daily chart as at August 28

Based on the above, I believe Ann Joo to be a good LT investment.

No comments:

Post a Comment