Magnum is the operator of the 4-D numbers forecast betting games which is sold through its 64%-owned subsidiary, Magnum4D. In the past two years, Magnum’s 4D games had been plagued by high prize payout ratio, which has affected the profitability of Magnum & Magnum4D.

Magnum & Magnum4D have just announced their 2Q2006 results ended 30/6/06. The results show good improvement in the result of both companies. The run of “bad luck” may have ended. In addition, the 2 companies have also benefited the introduction of Mbox game on April 1, 2006.

In the first part of this 2-part report, I shall look at the result of Magnum4D & its potential.

Current Financial Performance

Magnum4D reported an improved performance for 2Q2006. It managed to chalk up a net profit of RM37.1 mil as compared to a loss of RM8.8 mil recorded in the corresponding quarter last year. Turnover has also increased by 17.8% y-o-y to RM577 mil from RM490 mil previously.

Comparison of second quarter and first quarter can often be misleading because Magnum, like other gaming companies, normally enjoys better sale during the lunar New Year period. Nevertheless, it’s encouraging to note that the turnover for 2Q2006 has dropped by only 3.0% q-o-q as compared to a 14.3% q-o-q drop in the turnover for 2Q2005. The main reason for this is the introduction of Mbox game on April 1, 2006. This coupled with a lower prize payout ratio has helped Magnum4D to report a net profit of RM37.1 mil vs. a loss of RM24.0 mil incurred in 1Q2006.

Valuation

Assuming prize payout ratio & turnover remain similar to that of 2Q2006, Magnum4D can be expected to report a pre-tax profit of RM176 mil for a full year i.e. 2Q2006 pre-tax profit of RM44 mil multiplied by 4. Net profit will work out to be about RM126.72 mil i.e. RM176 mil multiplied by a factor of 0.72. EPS will be about 76 sen!!!

As always, when confronted with such high number, I will discount it by 30% to arrive at the “final” EPS of 53.2 sen. Based on this morning session’s closing price of RM2.52 & an EPS of 53.2 sen, Magnum4D’s PE is now only 4.7 times. That’s very cheap for a gaming stock.

PS. I've decided to ignore the net profit figure for 2Q2006 because the effective tax rate of 16% is too low. There may be good reason for this but we cannot expect the same to prevail in other quarters.

Technical Picture

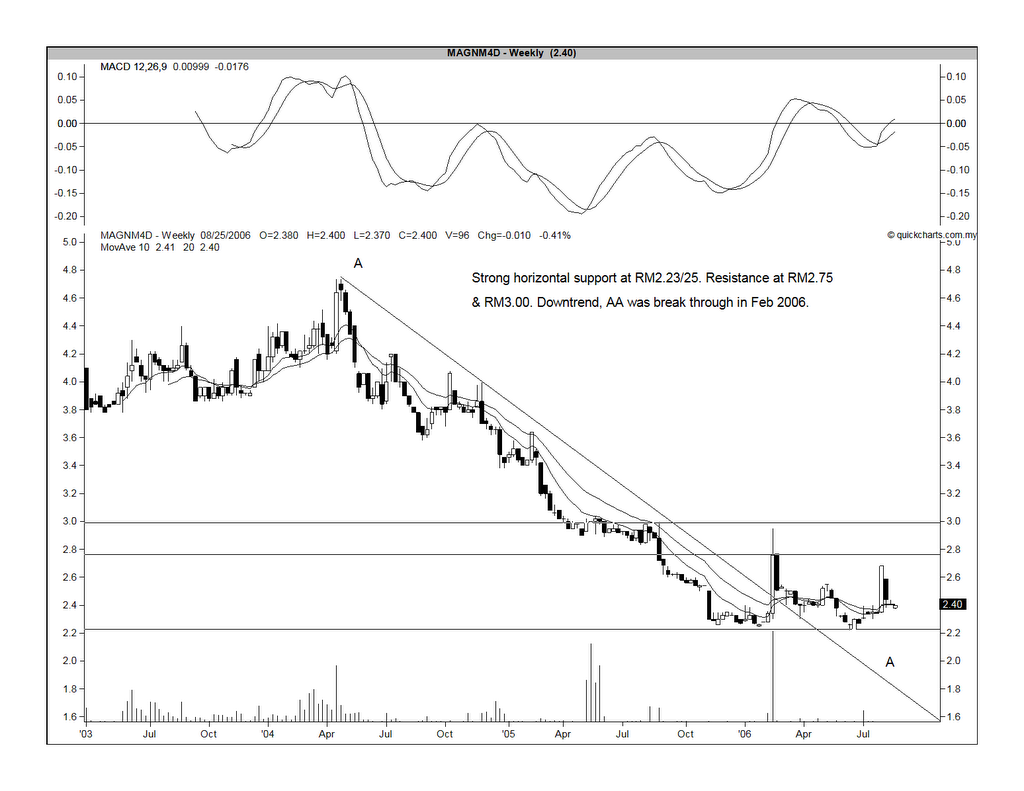

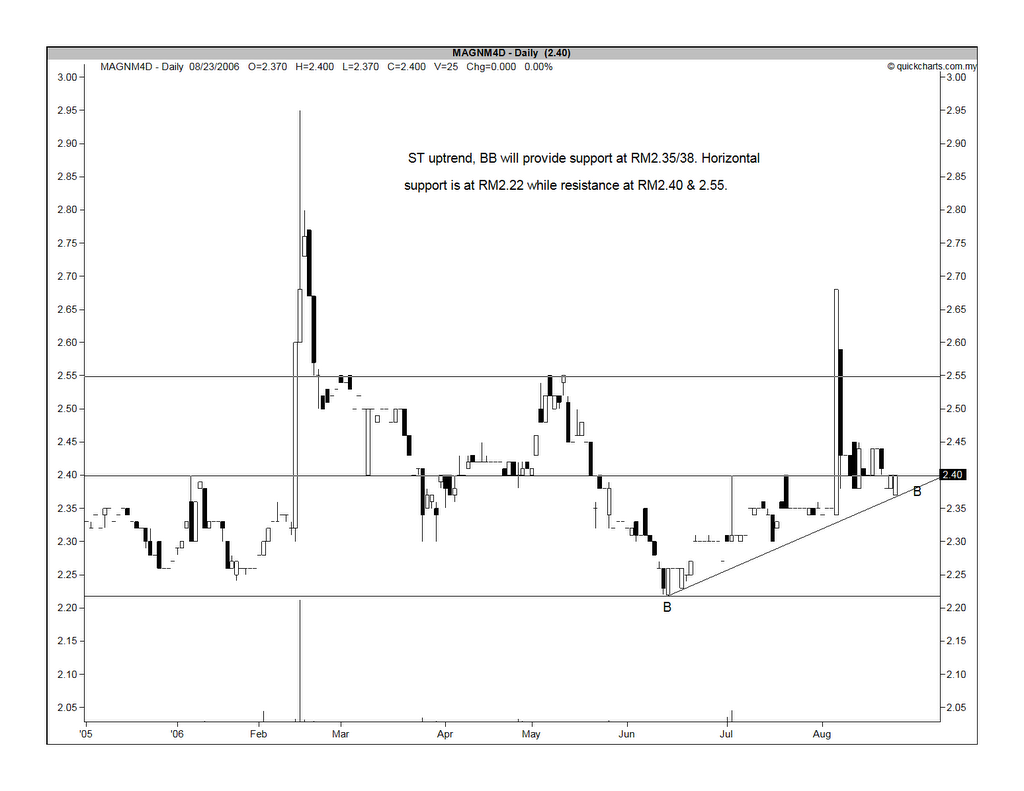

Magnum4D has broken out of its downtrend line at RM2.40 in w/e Feb 17, 2006. Since the breakout, it has been moving sideway (see Chart 1 below). From the daily chart (Chart 2), we can see that Magnum4D is in a ST uptrend, with support at RM2.38.

Chart 1: Magnum4D's weekly chart as at August 23

Chart 2: Magnum4D's daily chart as at August 23

Recommendation

Based on cheap valuation & good technical set-up, I believe Magnum4D to be an excellent investment choice.

No comments:

Post a Comment