For the full year ended 30/6/2006, net profit increased 12.0% to RM2.804 billion on the back of a 13.3%-increase in turnover to RM12.702 billion. The bank has attributed its good performance to its 3-pronged strategy, namely to diversify the income streams to include other non-banking income; to improve revenue from overseas operations; and, to grow non-interest income. The non-banking income came substantially from MNI, which became a subsidiary of Maybank after the bank acquired 73.62% of MNI on Dec 13, 2005. The stake was increased to 100% on May 17, 2006.

Valuation

Based on the latest quarterly EPS of 22.54 sen for 4Q2006, we can compute the full year EPS as 90.16 sen. This may appear high when compared to its 2006 EPS of 74.43 sen but I believe otherwise. This is because Maybank can expect to benefit from full year contribution from MNI as well as greater contribution from its fast growing overseas operation. Based on the EPS of 90 sen and yesterday's closing price of RM10.80, Maybank is now trading at a PE of 12 times. I believe that is very attractive for the prime banking group in this country.

Technical Picture

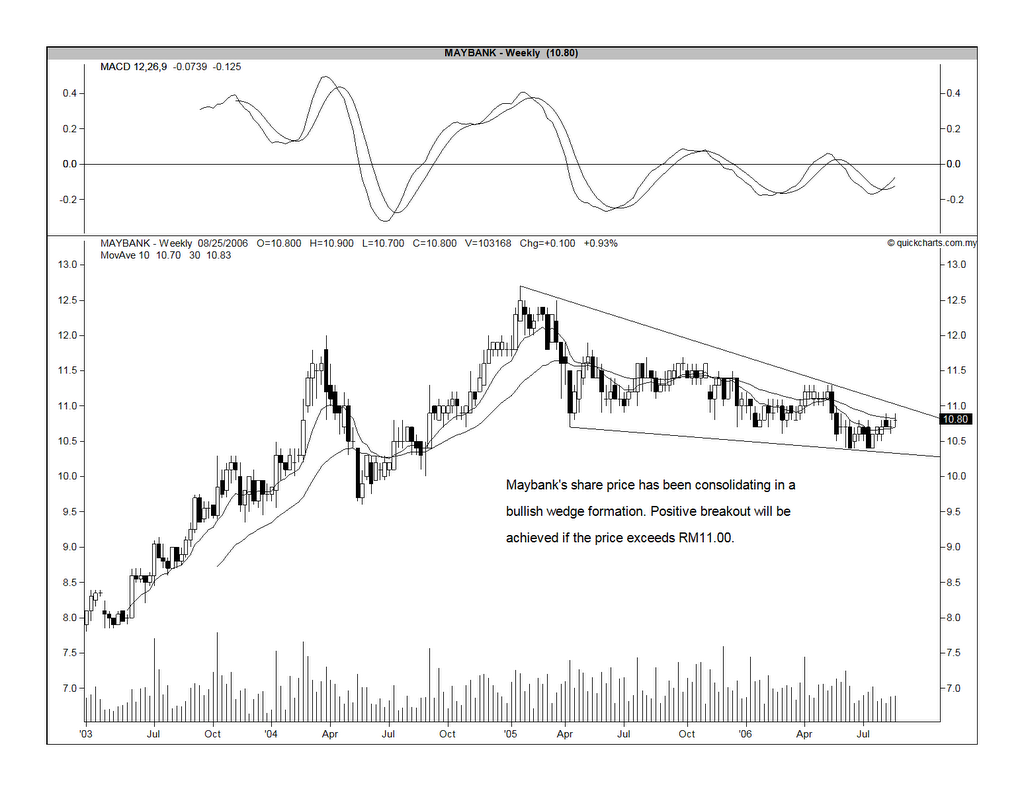

Maybank has been consolidating since January 2005, when it achieved an all-time high of RM12.70. The share is trapped in a downward sloping wedge (also known as a bullish wedge because it tends to break on the upside). The breakout, if it happened soon, would be at RM11.00. At the end of the morning session, the share closed at RM10.90, gaining only 10 sen. See chart 1 below.

Chart 1: Maybank's weekly chart as at August 24

Alternative instruments

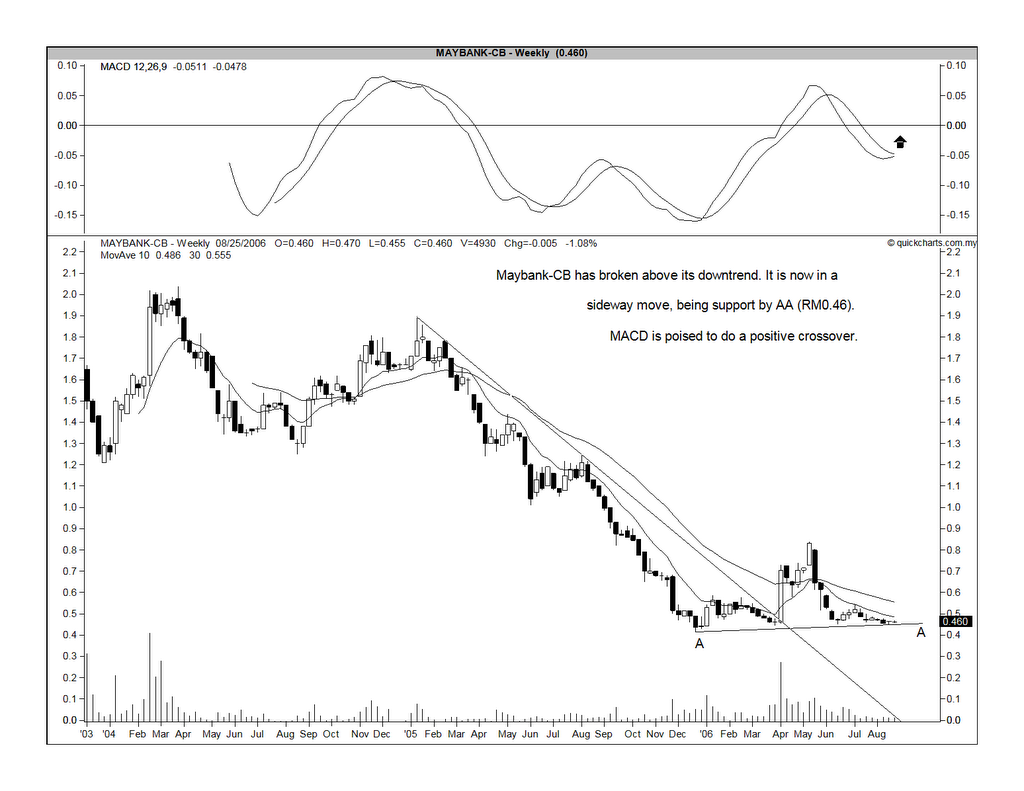

Besides the share, one can gain exposure to Maybank by buying into 2 covered warrants i.e. Maybank-CA & Maybank-CB.

Prices as at August 24, 2006

From the above, you can see that Maybank-CA is more attractive as it is trading at a discount of 0.6% while Maybank-CB is trading at an undemanding premium of 5.1% only. Techncially speaking, Maybank-CB is a safer buy as it has broken out of its medium-term downtrend and it is now moving sideway, with good horizontal support at RM0.46. MAybank-CB is still in a downtrend but it seems to have a good aupport at the psychological RM1.00 support level.

Chart 2: Maybank-CA's weekly chart as at August 24

Chart 3: Maybank-CB's weekly chart as at August 24

Recommendation

Based on the above, Maybank looks like a good investment especially if it breaks above the RM11.00 resistance. If so, you may also like to consider the 2 covered warrants, Maybank-CA & Maybank-CB.

No comments:

Post a Comment